6 Data Driven Reasons Why Micron Has 20% Upside

What You’ll Learn

- DRAM generates huge amounts of FCF.

- Fundamental metrics are pointing in the right direction with valuation multiples showing that MU is not expensive.

- Business risks exist with MU.

- Fair value from $58 to $75 with average fair value of $66.

In case you missed it, here’s what happened in Q2.

- Revenues of $7.35B, up 58% vs same period last year

- Operating cash flow of $4.35B vs $1.77B for the same period last year

On a table, it looks like this. Check out the margin expansion from just one year ago.

There are plenty of naysayers with Micron (MU), but the company is proving them wrong. This type of sales increase has fueled the company’s SSD market share and as the world continues to digitize, Micron is taking advantage of growth initiatives in:

- high end smartphones

- AI smart cockpits

- higher demand in datacenters

This is a capital intensive business, yet management created $2.2B positive FCF. This is the type of cash generation a company like Tesla would dream of.

Growing DRAM And NAND Industry

I like to buy cheap stocks. Who doesn’t love a good bargain, and if it works out, that feeling is awesome.

It’s even better if the industry outlook is also favorable to provide tailwinds.

Industry growth alone is projected to be 20% for DRAM and 45% for NAND. A lagging company in this industry would be buoyed by such industry growth, but if a company is projecting to be in-line or above industry growth, that is a big plus.

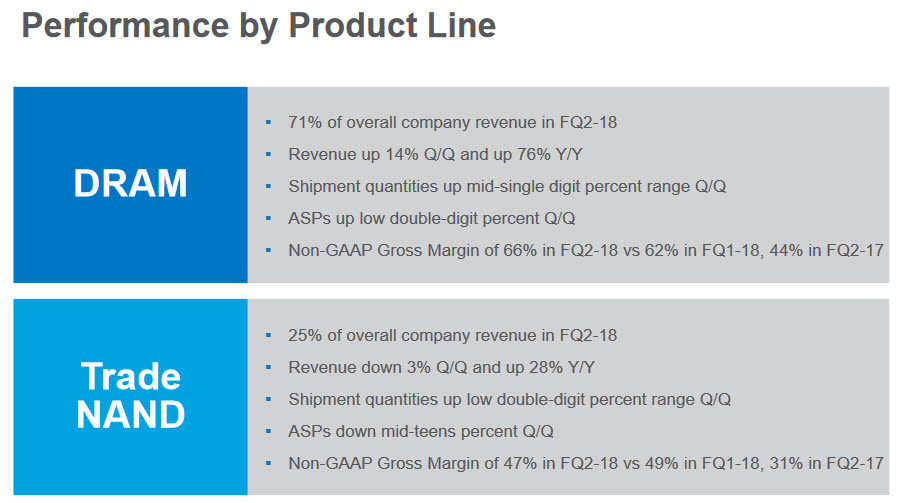

Highlights of DRAM and NAND business lines below.

{kind=link}

{kind=link}

NAND is slightly down on a quarter over quarter basis, but up 28% year over year. There’s room for improvement in the NAND division, but if they can hit on 45+% growth as they are projecting, things will look good.

But how does all this translate to whether Micron is a buy at these levels?

Deep Fundamental Look at Micron

On a quick surface level, Micron caught my eye with some cheap stats:

- PE of 6.4

- EV/EBIT of 5.4

- FCF positive with P/FCF of 8.8

- Increasing ROE to 39%

- Increasing CROIC to 20%

It’s currently sporting the cheapest and best numbers since 2010.

In this chart, I put together, I put P/FCF, ROE and CROIC over each other to see how healthy the fundamentals were compared to the stock price.

source: Barcharts and Old School Value Key Stats

I was hoping that the signs would be clearer, but not so much. All I know for sure is that 2010 was a great to buy and hold, and 2018 TTM Micron offers a impressive fundamentals with a cheap P/FCF.

Does Micron Pass the Quality Test?

So far, Micron looks cheap.

But is the company good enough to continue growing? Semiconductor’s aren’t known to have a lasting competitive advantage. Moat is very small. Competitors can outrun you if make a mistake.

One way to do a simple and quick quality check is to analyze the Piotroski score.

All those ups and downs confirm that Micron doesn’t have a moat. So that’s one strike against it for long term investors.

However from a quality standpoint, it’s scoring 7 out of 9 in the Piotroski score which is a good range to be in. Currently the business is running well and if they can continue to grow with the market, signs are pointing in the right direction.

Inventory Snapshot Show Anything?

Not all inventory is created equal.

For any company that makes things, I take a look at the make up of inventory to search for any red flags that management is not talking about or trying to hide.

Process is simple.

- compare revenue growth to accounts receivables

- compare the different types of inventory

Click to enlarge. Source: Old School Value Inventory Analysis.

The big increase in AR in 2017 is alarming, but it is balanced with the revenue growth. Otherwise, it would have been a big red flag. TTM figures balance things out. Step 1 is a pass.

In Step 2, you can see that raw materials are increasing which is great. Companies buy raw materials to prepare for demand or if the cost is low and they want to stockpile.

Works in progress have only slightly increased. Could signal slower growth than FY 2017.

Finished goods are up only slightly meaning they have enough in stock to meet demand. There is no big burst of demand at this time.

No red flags in the inventory and there aren’t signs of decreased demand from the latest TTM numbers.

Red Flags to Watch For

So far so good, but that doesn’t mean there are no risks.

The obvious so far is that Micron is a capex business and cyclical. If that’s not your thing, then it’s easy to pass and move onto something that suits your taste.

Excess Inventory

Price cuts can come quickly and hard in this industry.

If competitors like Samsung and Hynix build too much inventory and slash prices, Micron will have to follow suit.

In Q2, Micron decreased average selling prices of per gigabyte for NAND products by the mid teens range. That’s quite a drop.

International Trade Risks

Micron has been bouncing around as it does a significant amount of business outside the US. Last year, 86% of revenue was non-US sales. With manufacturing concentrated in Singapore, Taiwan, Japan and China, trade wars, higher taxes could spell trouble for Micron.

As there is no way to protect yourself risks outside the company’s control, the best thing you can do is buy it at a cheap price and give yourself margin of safety.

Fast Product Cycle

Semiconductors are becoming more complex. More demands, more research, more testing, more debugging, expensive manufacturing, short life cycles.

source: McKinsey&Company

With so much investment required for each product, the company has to get it right. You saw what happened with AMD and Nvidia. Both companies were coasting along the bottom, until demand hit, their product lines improved and the stock price followed.

If Micron gets it right, it will reap returns. One misstep can potentially mean another 1-2 years of losing money while Samsung and Hynix eats it all up.

So What’s it Worth?

This wouldn’t be complete without trying to get a fair value range.

Based on the information, industry growth, risks and other things I’ve gone through here, I have entered adjustments into the 4 valuation models I use to come up with an average.

Rather than go through all the details of each valuation method, I’ve written a how to value stocks series in the past that you can read up on.

Here, I use 4 valuation methods to come up with a range and an average value.

- DCF

- Graham’s formula

- EBIT multiples

- Absolute PE

With my adjusted inputs, the fair value range is from $58 to $75. It’s a wide range, but better reflects the realities of where the value lies. It’s better to be approximately right, than precisely wrong.

The Graham and EBIT valuation are much higher because the projected earnings and revenue is much higher than historical growth numbers. If Micron hits those numbers, you’re looking at mid to high $70’s.

The stock has run up, but at current prices relative to the value and fundamentals, it looks to be fairly valued. Not expensive as some might think.

With an average fair value of $66, there’s only a 15% margin of safety. That’s something to think about if you want to protect your downside.

Summary

- DRAM generates huge amounts of FCF.

- Fundamental metrics are pointing in the right direction with valuation multiples showing that MU is not expensive.

- Business risks exist with MU and quality durability is spotty.

- Fair value from $58 to $75 with average fair value of $66.

Disclosure

No positions in any stocks mentioned, but may initiate a long position in MU over the next 72 hours.